How to stick to your financial New Year’s resolution

Looking for advice on how to keep to your New Year's resolution? Here are our tips on how to stick to the most common financial goals aimed for in the UK.

It’s that time of year again. New Year’s around the corner and everyone’s thinking about what they want to do in the coming 365 days. Whether that’s finally getting fit or learning that instrument you’ve had your eye on, most people would agree that they make at least one New Year’s resolution.

But how likely are you to stick to your New Year’s resolution, and we mean actually stick to it? It may be that you have the willpower to follow through on your decision, but for many of us, finishing our resolution can be tricky, especially if it’s financially based.

So, to find out just how likely Brits are to stick to their resolution, we carried out a survey to see how many of us realise our financial New Year’s ambitions.

From our data, we found out how long people stick to their resolutions, why they want to try them, what the most popular financial resolutions are, and the biggest challenges facing their completion.

Be sure to stick around till the end for our tips and tricks for sticking to your financial resolutions.

What are the most popular financial resolutions?

To start with, let’s break down what the most popular financial resolutions are in the UK.

Right at the top, 42% of people say that they want to set a savings goal and hit it, while 31% want to stop frivolous spending – two things that we can all relate to. Alongside this, 31% also state that they want to be financially comfortable in the coming year, which makes sense given the cost of living crisis.

In other cases, 28% say they’re aiming to pay off a debt or credit card that’s getting out of hand, while 19% want to be more comfortable paying their bills, and 16% have a bad credit score they want to improve. In fact, bills were a very common theme, with a further 12% wanting to get up to date with their energy bills as soon as possible.

Besides these goals, 11% set themselves the simple challenge of regularly checking their credit score, while another 6% want to save for a mortgage deposit. Finally, 8% say they want to buy a new car, whether through a lump sum payment or car financing.

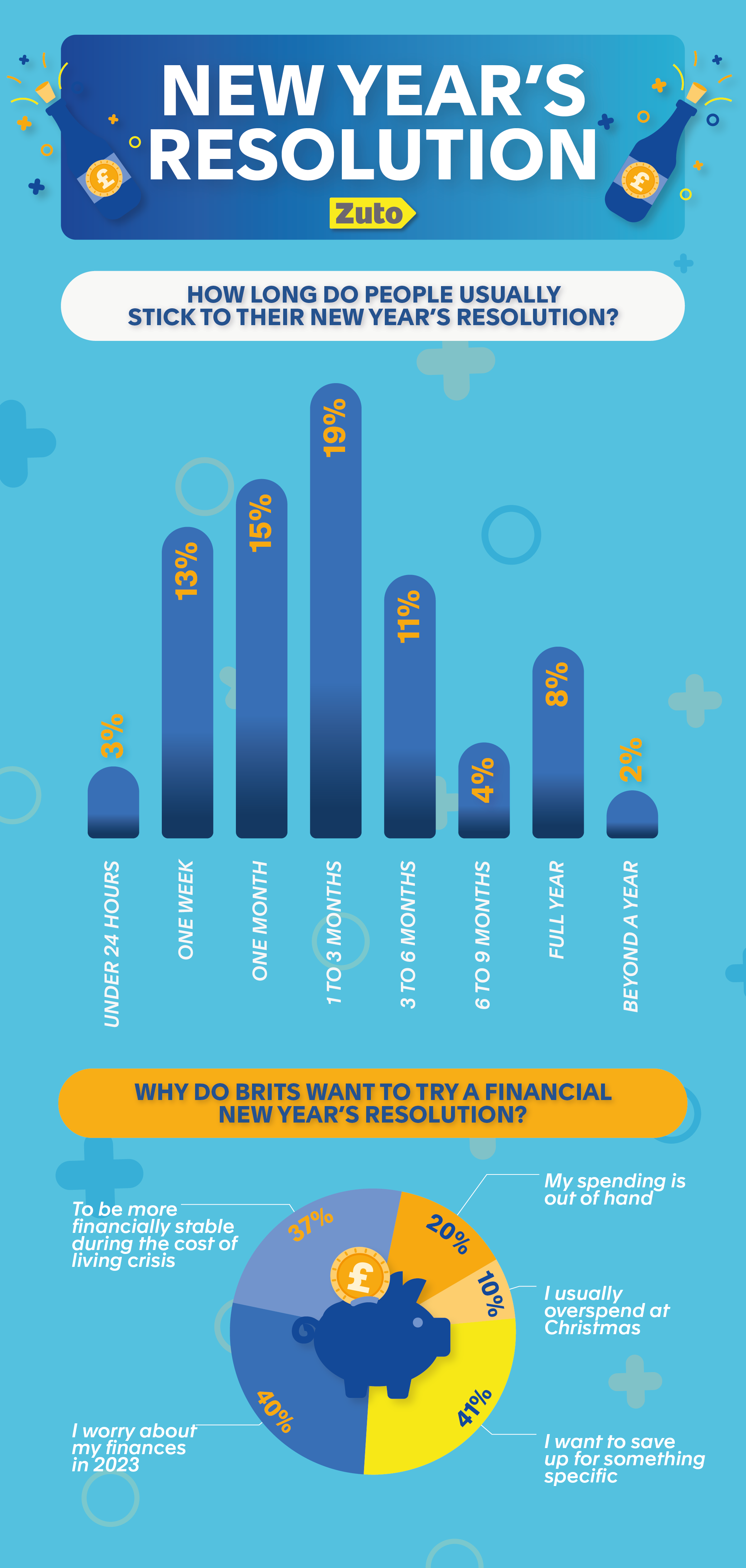

How long do people stick to their New Year’s resolutions?

Perhaps it should come as no surprise that 19% of people give up on their New Year’s resolution after little more than one month, with one to three months being the most common average. In many cases, however, one month is just as likely, with 15% of those we surveyed giving up after this point.

As for shorter periods, 13% of those we spoke to say they ended their resolution after just one week, while 3% gave up after just a single day! Only 4% of those we spoke with say they kept their resolution for six to nine months, and just 8% managed to stick to their plan for a whole year.

In other words, sticking to a New Year’s resolution is hard.

Why do people want to try financial resolutions?

For many of us, getting control of our finances is a long-term goal that can take several years to achieve. After all, there’s a lot that goes into levelling out your finances, and in many cases, there are things outside of our control that can affect our ability to save.

For the majority of those we surveyed, 41%, their aim was to save up for something specific, such as a car or their first home. On top of this, 40% of people say they’re worried about how their finances will look in 2023, which again comes as no surprise.

In other cases, 20% of those who responded to our survey pointed out that they feel their spending is out of hand or they simply want to challenge themselves to do better. And, naturally, some of those we spoke with agree that they always overspend at Christmas, with 10% looking to cut back on this.

What are the biggest challenges preventing people from achieving their resolution this year?

As we’ve mentioned, there are a plethora of things that can get in the way of us balancing the books, and this coming year is likely to be no different.

A full 45% of those we asked say the cost of living crisis is the biggest hurdle towards their financial goals. Alongside this, another 34% mentioned that they simply have a lack of self-control when it comes to their finances.

A further 27% point to ongoing economic instability as being the key obstacle in the way of their savings, while 19% admit that they’re not setting themselves reasonable saving targets. This is backed by our final point, which highlights 18% of those we spoke with as spending outside of their assigned budget.

How can you achieve your financial New Year’s resolution?

Before we share our top tips and trick for achieving your financial goals this coming year, we should point out that there’s no shame in failing to hit your New Year’s resolution. It’s a challenge, one that often puts a lot of pressure on us to complete.

With that being said, here’s how you can start working towards achieving the most common financial resolutions we pick.

1. Setting a savings goal and achieving it

One of the most important things to do when it comes to setting and meeting a savings goal is to set a savings cap that is achievable.

If you know that you’ll only be able to put a little bit of your wage away at the end of each month, then there’s no point trying to save thousands of pounds.

Instead, focus on setting a savings goal that works for you. To see what’s reasonable, start by tracking what you spend on average in a month, and work what your essential outgoings are. That could mean rent, gas and electric bills, monthly car payments, travel costs or anything else that you’ll need to budget for regularly. When you know what your essential monthly outgoings are, you’ll know how much you’ll be left with, and from there you can set a sensible amount to put into your savings each month while still making sure the essentials are covered.

2. Stopping frivolous spending

Okay, this one can be rather tricky, especially if you find money burns a hole in your pocket. It’s reliant on your willpower and planning more than anything to stop you from spending.

When buying anything, the first thing you should be asking yourself is whether or not you actually need what you’re about to buy. If the answer is no, then put it down and walk away. We know this is tricky, but once you get used to it, you’ll find your spending habits starting to change naturally.

Of course, there are also other little things you can do to cut unnecessary spending. Take a look at all your current subscriptions and cancel any that you don’t use or need. You can also unsubscribe from marketing emails to remove the temptation of browsing new offers, and leave credit and debit cards at home if you don’t need to shop while out.

And if you’re really struggling with this, then banking apps like Monzo and Revolut have features you can use to track and monitor your spending.

3. Improving a bad credit score

If saving isn’t the issue but you do find yourself in need of financing for certain large purchases, then you likely know how important your credit score is for getting a good deal.

The good news is that, while slow, you can improve your credit score. If you want to find out how, you should read our article on how to improve your credit score in 15 steps.

As for the goal of checking your credit score more, you can actually check your score as often as you like with no negative impact. You can check your score with the three main credit reference agencies - TransUnion, Equifax, and Experian.

All you need to do after setting up an account to check your credit score is to get in the habit of checking it once a month. This can be easily facilitated by setting a monthly reminder on your phone.

4. Paying off your debts

It can be hard to know where to start when it comes to paying off your debts.

To begin with, you could target any debts you have with high interest rates. Interest means you pay more, so getting these debts resolved first can help to save you money in the long run. It might take a while to sort out if you’ve got a lot of different debts, but as a bonus, clearing your debts can help to boost your credit score as well as help you save.

As for credit cards, try to avoid maxing them out whenever possible. Try not to spend over 30% of your card limit at any one point and always aim to pay them off as soon as possible.

If paying off your debts is going to be tricky for you in the new year, consider looking at refinancing options for your credit products. Switching to a longer payment term can help to reduce your monthly payments, or check to see if you’re now eligible for a lower rate.

5. Paying your bills

Meeting all your bills next year might very well be a challenge, especially given the current cost of living crisis. Much of the advice we can offer relates to spending less and prioritising your bills alongside other essentials, along with some of the other money-saving tips we’ve mentioned.

Unfortunately, the hard truth is that by meeting your bills, you will most likely be forced to sacrifice other luxuries, though this is more than worth it in the long run as you’ll avoid getting into unnecessary debt by missing bill payments.

6. Being financially comfortable

Last, but not least, we have the goal of being financially comfortable in the New year, and as with meeting your bills, this all comes down to how you approach saving and spending.

In many cases, by following the advice we’ve outlined above, you’ll find your financial situation stabilising, though it might take longer than a year before you find yourself in a position of being financially comfortable.

However, if you want a sense of financial comfort as soon as possible, you could set aside what’s known as a safety fund. This pot of money can be used to cover unexpected financial pressures, meaning you don’t have to dip into your savings unless absolutely necessary, allowing you to keep saving.

We really don’t need to mention again just how tricky it can be to follow through on a New Year’s resolution, especially a financial one, but with our list of tips to hand, you should hopefully find the process of improving your financial situation that much easier.

Of course, if your New Year’s goal is to buy a new car, then the team at Zuto might be able to help. We’re experts in the field of car finance, including bad credit car finance, and can offer you a flexible and financially viable way to buy your next car.

Get in touch with us today to see how we might be able to help you and don’t forget to check out our blog for more pieces like this one.